The MSP market is evolving beyond simple consolidation into a more capital-backed platform model. As acquirers pursue growth in security, ERP, and automation, M&A is becoming a clearer signal of where the channel is headed. This blog explores what that means for the future of the MSP ecosystem.

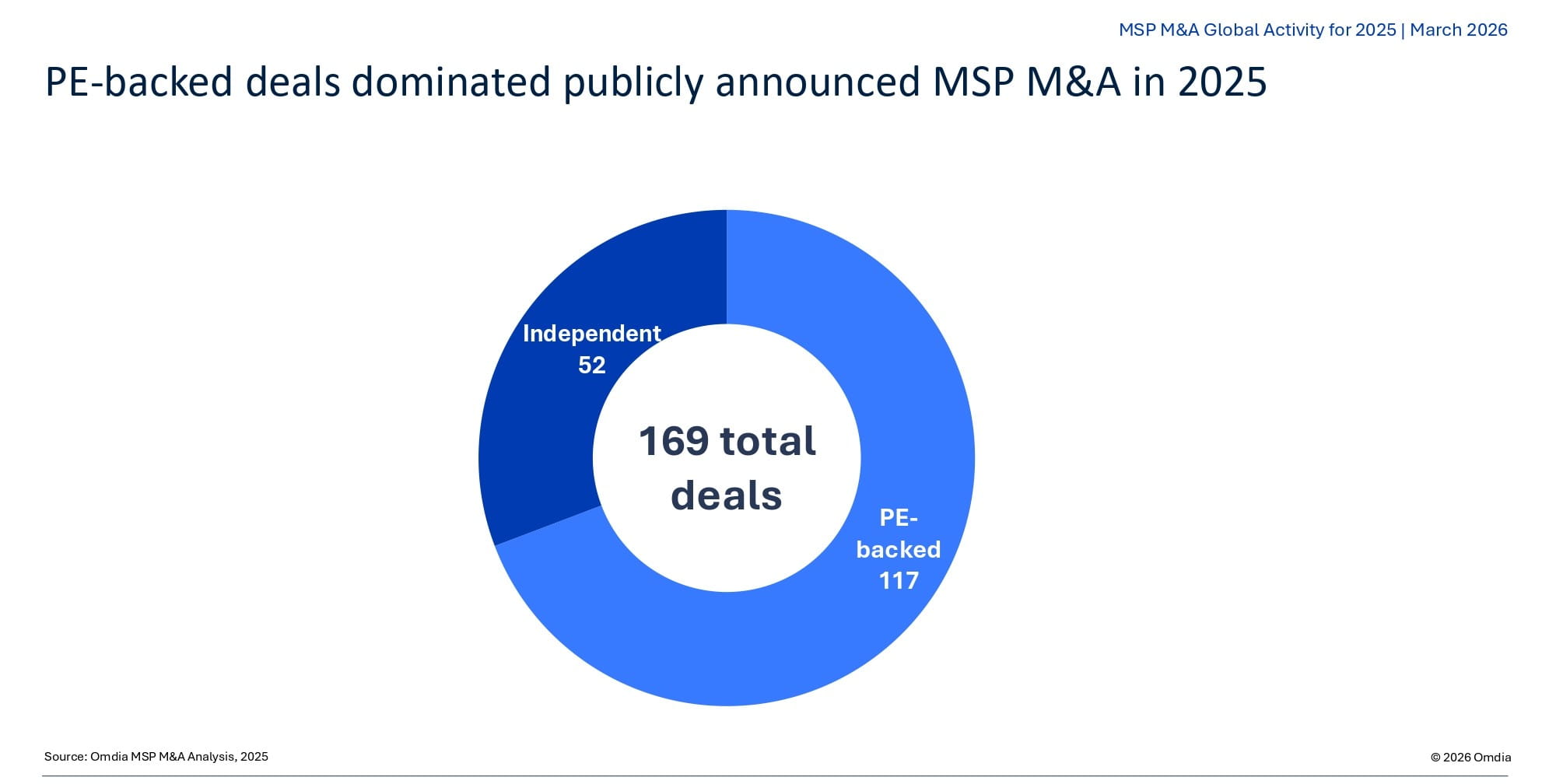

Omdia tracked 169 publicly announced MSP-related M&A transactions in 2025. On the surface, that confirms what the channel already knows: consolidation continues. But the more important story is not volume. It is structure.

Private equity appeared in 69% of the disclosed deals. That percentage likely overstates true PE participation, since smaller MSP-to-MSP transactions are less frequently announced. Even with that caveat, institutional capital remains deeply embedded in the visible market.

What has shifted is the nature of participation. The market has moved beyond one that has a leading edge defined by first-time roll-ups. In 2025, new platform launches sat alongside recapitalizations, where one sponsor exited and another stepped in. That matters. It signals that MSP platforms are maturing into assets capable of supporting multiple ownership cycles. The MSP channel is not simply consolidating; it is becoming institutionalized.

At the top of the acquirer rankings, activity concentrated among a handful of repeat buyers. Evergreen Services Group (Alpine Investors) led by deal count, operating through both its Lyra MSP arm and Pine Services ERP arm. Behind it sat a second tier of active platforms, each pursuing a distinct integration approach.

Deal count alone, however, is not the only differentiator. The dividing lines are increasingly defined by operating thesis.

Some platforms continue to emphasize geographic density and scale across smaller MSP targets. Others are expanding into adjacent capabilities such as managed security, ERP implementation, and vertical specialization. A smaller but visible set is organizing around automation and AI as the core of the delivery model itself.

In other words, the strategic intent behind acquisitions is becoming more varied.

Security remains one of the clearest capability drivers. Seventeen transactions in 2025 involved MSSP targets. Some were MSSP-to-MSSP combinations, reflecting consolidation within the managed security segment itself. Others saw MSPs acquiring security specialists to embed cyber capabilities directly into their service portfolio.

This trend reinforces what vendors already understand: cybersecurity is no longer an optional add-on. It is increasingly expected within the managed services contract. Acquisition is simply the fastest path to closing capability gaps.

ERP and application expertise represent another layer of expansion. Multiple deals involved ERP-focused partners, particularly within the Acumatica, Sage, NetSuite and SAP ecosystems. These transactions suggest that certain MSP platforms are looking beyond infrastructure management toward higher-margin, application-centric services. That shift has implications for both vendor alignment and talent strategy.

Geographically, consolidation remains largely domestic. Of the 169 tracked deals, 95% occurred within the same region as the acquirer. North America accounted for three-quarters of acquirer-side activity, with EMEA and APAC following. Cross-border expansion was selective and primarily driven by well-capitalized platforms.

That regional concentration indicates that regulatory alignment, labor models and customer density continue to anchor most strategies locally. International expansion is deliberate rather than opportunistic.

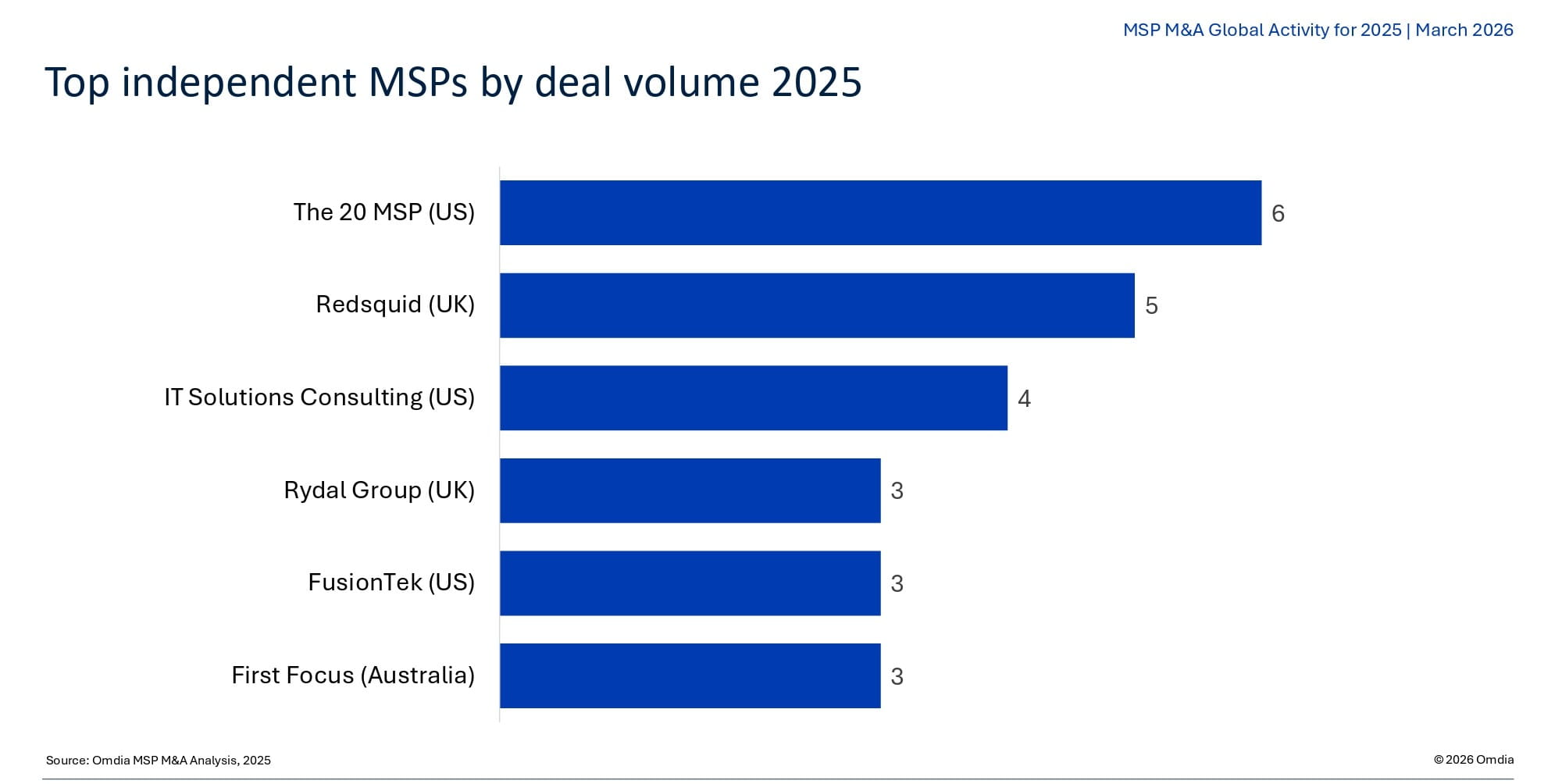

The presence of independent buyers also remains meaningful. Fifty-two deals involved no PE participation. Firms such as The 20 MSP, Redsquid, IT Solutions Consulting and others continued to build through acquisition without institutional capital backing. While less visible than sponsor-backed platforms, these players form an important layer of the market’s growth story.

Taken together, the 2025 data points to a market that is stratifying.

On one end is the long tail of fragmented local providers. At the other end are increasingly capitalized platforms making centralized procurement and integration decisions. Between them lies a spectrum of operators pursuing targeted growth.

For technology vendors with MSP go-to-market strategies, this shift is material. As ownership consolidates, procurement authority concentrates. Vendor selection decisions are more likely to be standardized across multi-region platforms. That increases both the upside of winning a platform relationship and the downside of losing one.

At the same time, the emergence of automation-first platforms hints at a different axis of competition. If service delivery increasingly hinges on workflow automation and centralized data visibility, then margin structure, not just revenue scale, will define competitive advantage.

The headline number, 169 deals, confirms that consolidation continues. The deeper signal is that the MSP ecosystem continues to evolve into a capital-structured platform market differentiated by thesis, capability mix and operating model.

More from author

More insights

Assess the marketplace with our extensive insights collection.

More insightsHear from analysts

When you partner with Omdia, you gain access to our highly rated Ask An Analyst service.

Hear from analystsOmdia Newsroom

Read the latest press releases from Omdia.

Omdia NewsroomSolutions

Leverage unique access to market leading analysts and profit from their deep industry expertise.

Solutions